How to Start a Budget (Step-by-Step)

Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you.

Starting a budget does not need to feel overwhelming. The goal is to build something easy enough to follow consistently while still giving your money some structure.

A good budget helps you see where your money is going, stay on top of bills and spending, and make progress toward savings goals without feeling overly restrictive.

The steps below walk through a straightforward way to build a budget using your real income, real spending habits, and a setup that can adjust as life changes.

Read Best Investment Apps to see our top picks.

How to Start a Budget

Starting a budget does not need to feel complicated. The goal is to build something you can realistically follow without constantly adjusting or restarting it.

A good budget helps you understand where your money is going, stay on top of bills and spending, and make steady progress toward savings goals without feeling too restrictive.

The easiest way to start is to:

- Figure out how much money you bring in each month

- List your main expenses

- Organize your spending into a few simple categories

- Make small adjustments as you go

The steps below walk through a practical way to build a budget based on your actual income, spending habits, and everyday routine.

Step 1: Calculate Your Monthly Income

Start with the amount of money you actually bring home each month — not your salary before taxes or deductions. This gives you a more realistic starting point and helps keep your budget from breaking down right away.

When calculating your income:

- Use your take-home pay after taxes

- Include only income you can rely on consistently

- Leave out bonuses or irregular income for now

If your income changes month to month, use your lowest normal month as your baseline. One simple way to do this is to look at your lowest 1–2 months from the last six months and build your budget around that number.

That gives you more breathing room during slower months and lowers the chances of overspending when income drops unexpectedly.

Before moving on, make sure you know how much money is actually available each month. Every part of your budget depends on that number.

If you are setting up your accounts from scratch, it also helps to understand how many bank accounts you should have and how to organize them.

Step 2: List Your Fixed Monthly Expenses

Next, list the expenses you have to pay every month. These are the bills your budget needs to cover first before you start planning for anything else.

Common fixed expenses include:

- Rent or mortgage

- Utilities

- Insurance

- Phone and internet bills

- Subscription services

- Minimum debt payments

These costs usually make up the core of your budget because they are harder to reduce or adjust quickly.

If some bills change slightly from month to month, use a rough average from the last few months instead of trying to get every number perfect.

At this stage, you just want a clear picture of how much of your income is already spoken for before moving on to everyday spending.

Step 3: Estimate Your Variable Expenses

After fixed bills, look at the spending that changes month to month. This is usually where budgets start getting off track because smaller purchases are harder to notice in the moment.

Variable expenses often include:

- Groceries

- Gas and transportation

- Dining out

- Shopping

- Entertainment

- Personal spending

If you are not sure what you normally spend, check your last 1–2 months of bank or card transactions instead of trying to estimate from memory. Most people spend more in these categories than they realize at first.

A simple way to do this is to:

- Open your banking app

- Review the last month of transactions

- Add up rough totals for your main spending categories

You do not need exact numbers right now. You just want a budget that reflects how you actually spend money so it feels realistic enough to stick with.

Step 4: Set Simple Spending Categories

Now organize your spending into a few simple categories. The goal is to make your budget easy to follow without creating something that feels annoying to keep up with.

A basic setup usually works well:

- Needs — housing, utilities, groceries, insurance

- Wants — dining out, entertainment, shopping

- Savings and goals — emergency fund, investing, debt payoff

You do not need a huge list of categories to make a budget work. For most people, broader categories are easier to manage and make it simpler to adjust spending when needed.

One common starting point is the 50/30/20 budget, which splits income into needs, wants, and savings. The exact percentages matter less than having a structure that helps you quickly see where your money is going.

Step 5: Build a Flexible Budget Plan

Now it is time to put everything together into a budget you can realistically follow month to month.

One of the biggest budgeting mistakes is making the plan too strict right away. When unexpected expenses show up — even something small like a higher grocery bill, car repair, or extra night out — the budget starts falling apart.

A little flexibility usually works much better long term.

Some easy ways to make your budget easier to stick with include:

- Leave a small buffer in your budget

- Expect occasional unexpected expenses

- Let spending categories move around slightly when needed

Even a small cushion of $50–$100 can help absorb smaller surprises without throwing everything off.

The goal is not to make every category perfect. You just want a budget that can handle real life without constantly needing a reset.

Step 6: Track Your Spending Regularly

Once your budget is set up, the next step is paying attention to what you are actually spending during the month.

You do not need to track every dollar perfectly, but checking in regularly makes it much easier to catch problems before they get out of hand.

A simple routine usually works best:

- Check your accounts a few times per week

- Watch for categories getting close to their limit

- Make small adjustments before spending starts piling up

For most people, spending 2–3 minutes reviewing transactions is enough to stay on top of things without turning budgeting into a daily task.

The goal is not perfect tracking. You just want enough awareness to notice when spending starts drifting before it becomes a bigger issue.

Step 7: Adjust Your Budget as Needed

A budget is not something you set once and never look at again. Small adjustments during the month are what keep it working when life gets unpredictable.

Some months will cost more than expected. Other months will go more smoothly. What matters is making small changes as you go instead of waiting until the month is already off track.

A simple way to handle this is to:

- Review your budget once or twice per week

- Adjust categories if spending is running high in one area

- Make changes early instead of waiting until the end of the month

A lot of budgets fail because people treat them like a pass-or-fail test. In reality, budgeting works better when it feels flexible enough to adjust when needed.

If you want a simple way to organize budgeting, banking, saving, and investing together, you can see how the Savefinity System works here.

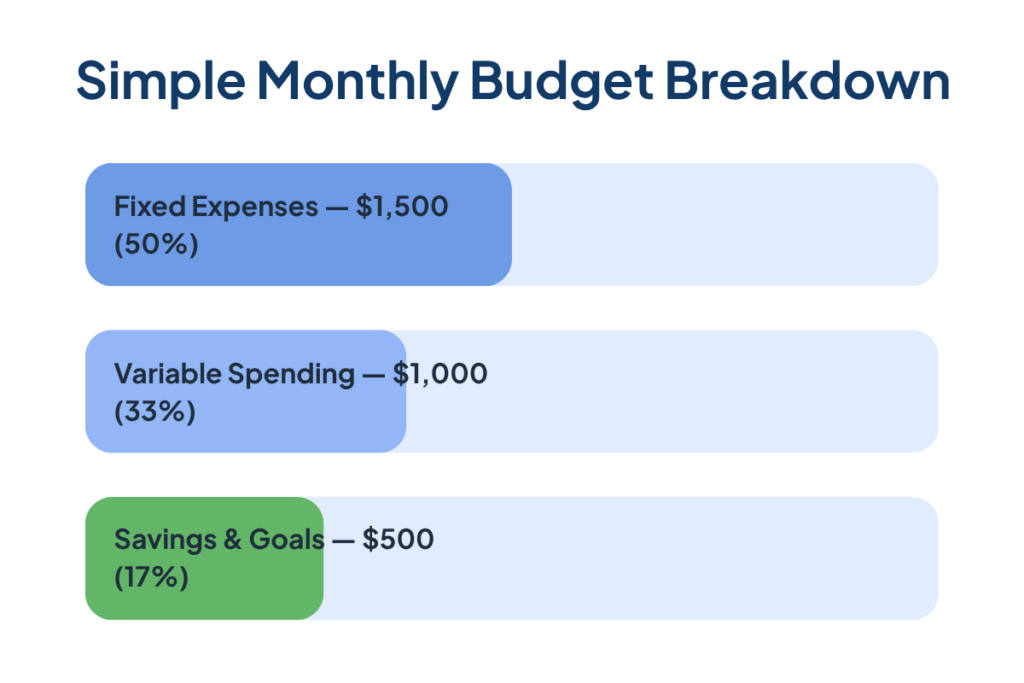

Example of a Simple Monthly Budget

Here is a simple example of what a beginner-friendly budget might look like using a $3,000 monthly income.

| Category | Amount |

|---|---|

| Fixed expenses | $1,500 |

| Variable spending | $1,000 |

| Savings and goals | $500 |

In this example, fixed expenses cover essentials like housing, utilities, insurance, and minimum debt payments.

Variable spending includes things like groceries, gas, dining out, and personal spending. This is usually the part of the budget that changes the most throughout the month.

Savings and goals can include emergency savings, investing, or extra debt payments. Treating savings like a regular monthly expense makes it easier to stay consistent instead of only saving money when extra cash happens to be left over.

If one category ends up running higher than expected, you can usually make up for it by cutting back a little somewhere else.

A budget like this does not need to be perfect to work well. The main goal is to give your money a basic structure that is easy to manage and adjust as needed.

Common Budgeting Mistakes to Avoid

Most budgeting problems do not happen because people are lazy or bad with money. Usually, the budget just becomes too difficult or frustrating to follow once normal life gets in the way.

Setting Spending Limits Too Low

A budget that is too restrictive usually falls apart pretty quickly.

If categories like groceries, gas, or entertainment are unrealistically low, it becomes much harder to stay on track once regular spending starts happening.

It is usually better to start with numbers that feel manageable and tighten things up later if needed.

Forgetting About Irregular Expenses

Expenses like car repairs, medical bills, gifts, or annual subscriptions can throw off a budget fast if there is no room planned for them.

Even a small buffer can help absorb unexpected costs without forcing you to restart everything.

Using Too Many Categories

Too many categories can make budgeting feel more complicated than it needs to be.

Most people do not need 15–20 detailed categories to manage their money well. A smaller number of broader categories is usually easier to track and maintain over time.

Not Checking Your Budget Regularly

A budget works much better when you check in consistently throughout the month.

Waiting until the end of the month to review spending usually makes it harder to fix problems before they get bigger.

Quitting After One Bad Week

Almost nobody follows their budget perfectly every month.

One expensive weekend or unexpected expense does not mean the budget failed. Making a few adjustments and moving forward is usually far more helpful than starting over from scratch.

A budget does not need to be perfect to work well. It just needs to be realistic enough that you can keep using it long term.

Should You Use a Budgeting App?

Read: How to Choose a Budgeting App to learn more.

A budgeting app is not necessary, but it can make budgeting easier once you already have a basic system in place.

Most budgeting apps help by:

- Tracking spending automatically

- Organizing purchases into categories

- Showing where your money is going throughout the month

This can save time and make it easier to stay aware of your spending without constantly jumping between bank accounts.

At the same time, an app will not fix a budget that already feels too complicated. In most cases, budgeting works better when the system itself stays simple.

For a lot of people, the best budgeting app is just the one that feels easy enough to keep using week after week.

If you want to compare different options, our guide to the best budgeting apps breaks down which apps work best for different budgeting styles and experience levels.

How to Start a Budget FAQ

How do I start a budget for the first time?

Start by calculating your monthly take-home income, then list your fixed expenses and estimate your variable spending. From there, organize everything into simple categories and adjust as you go. The goal is to build a basic structure you can follow consistently.

What is the easiest way to budget?

The easiest way to budget is to keep it simple. Use a few main categories, check your spending a few times per week, and make small adjustments when needed. Overcomplicating it is one of the main reasons budgets don’t last.

How much should I put toward savings?

There isn’t one exact number that works for everyone. A common starting point is around 10–20% of your income, but consistency matters more than the percentage. Even $50–$200 per month adds up over time if you stick with it.

What if my income changes every month?

Use your lowest typical monthly income as your baseline. This keeps your budget stable and prevents overspending during lower-income months. You can always adjust upward when you earn more.

Do I need a budgeting app to make this work?

No, a budgeting app isn’t required. Many people start with a simple setup using their bank account or a basic list. Apps can make things easier, but they work best when your system is already simple and clear.

How to Start Budgeting Successfully Long Term

Read Best Investment Apps to see our top picks.

Starting a budget does not need to be complicated to work. For most people, the budgets that actually last are usually the ones that feel realistic to follow during everyday life.

The goal is not to track every dollar perfectly or create a system that never changes. It is to understand where your money is going, stay aware of your spending, and make small adjustments before things start getting off track.

A good budget should help you feel more organized and more confident with your money without turning budgeting into something stressful or difficult to keep up with long term.