How to Choose the Right Bank

Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you.

Choosing a bank seems simple, but the wrong setup can quietly cost you through monthly fees, low savings rates, and accounts that make managing money harder than it needs to be.

The best way to choose a bank is to look at how you actually use your money day to day. Understanding how to choose a bank based on fees, account types, features, and accessibility can help you build a setup that is easier to manage while giving your savings more room to grow over time.

Many people choose a bank based on convenience or familiarity, but small differences in rates, automation, branch access, and account structure can make a noticeable difference long term.

Read: Best Banks for our top overall banking picks.

What to Look for When Choosing a Bank

A bank should match how you manage your money—not the other way around. If your setup feels confusing, slow, or annoying to deal with day to day, it’s usually not the right fit.

The easiest way to choose a bank is to focus on a few core things that affect how your money works over time:

- Type of bank

- Fees and savings rates

- Banking features and app quality

- ATM and branch access

These are usually the factors that determine whether a bank feels simple to use long term—or becomes frustrating to manage.

The best bank isn’t necessarily the biggest or most popular. For most people, the right setup is the one that keeps banking simple, avoids unnecessary fees, and works well with how they already manage money.

These are usually the factors that determine whether a bank feels simple to use long term—or becomes frustrating to manage.

| Factor | What to Look For |

|---|---|

| Bank Type | Online, traditional, or hybrid |

| Fees | No monthly fees or overdraft fees |

| Savings Rates | Competitive APYs |

| Features | Strong app, automation, transfers |

| Access | ATM network or branch access |

That’s usually enough to narrow down your options before comparing specific banks or accounts.

Types of Banks: Online vs Traditional Banks

One of the biggest decisions is choosing between an online bank, a traditional bank, or a hybrid option that gives you some of both. Each works differently depending on how you handle your money day to day.

If you want a deeper breakdown of the pros and cons, it helps to compare online vs traditional banks in more detail.

Online Banks vs Traditional Banks

Online banks are designed around digital banking. They often offer higher savings rates, fewer fees, and better mobile apps because they don’t operate large branch networks.

Traditional banks focus more on in-person service. That can be helpful if you deposit cash regularly, want face-to-face support, or like having a local branch nearby. The downside is that they often pay lower savings rates and may charge more account fees.

For a lot of people, online banks handle everything they need while keeping banking cheaper and easier to manage.

Here’s a quick look at how online and traditional banks usually compare:

| Feature | Online Banks | Traditional Banks |

|---|---|---|

| Savings Rates | Higher | Lower |

| Fees | Lower | Higher |

| Branches | No | Yes |

| Mobile App | Usually better | Varies |

In most cases, the biggest trade-off is convenience versus physical access.

All-in-One Banking vs Separate Accounts

Some banks let you manage checking and savings together in one connected setup, while others work better as part of a multi-bank system.

Keeping everything in one place is usually easier to stay on top of. Transfers are quicker, automation works more smoothly, and you don’t have to bounce between multiple apps just to track your money.

Separate accounts can still make sense, especially if you want the highest savings rates or specific account features. But they usually take more effort to keep organized over time.

When a Hybrid Bank Makes Sense

Hybrid banks combine digital banking tools with physical branch access. That can work well if you like online banking but still want access to branches once in a while.

This setup is often useful for people who deposit cash regularly, need wider ATM access, or simply prefer having the option to walk into a branch if something goes wrong.

The biggest thing to watch is whether that flexibility comes with lower savings rates or extra fees that are not really helping you.

For many people, online banks offer the best balance of low fees, convenience, and strong savings rates. But if branch access is important to you, a traditional or hybrid bank may be a better fit long term.

Compare Bank Fees and Interest Rates

A good bank setup usually comes down to two things: avoiding unnecessary fees and earning more on your savings.

| Weak Setup | Strong Setup |

|---|---|

| Monthly fees | No-fee checking |

| Low savings rates | High-yield savings |

| Multiple disconnected accounts | Connected banking setup |

| Manual transfers | Automatic transfers |

| Clunky mobile app | Simple mobile app |

Small differences in fees and savings rates can end up costing — or saving — more money than most people realize.

Even a modest monthly fee or a lower savings rate can quietly cost you hundreds of dollars over a year. In a lot of cases, this is the difference between a bank account that helps your money grow and one that slowly chips away at it. If you want to compare real options side by side, it helps to look at the best banks and see how they compare.

Common Fees to Avoid

- Monthly maintenance fees

- Overdraft fees

- Minimum balance fees

- Out-of-network ATM fees

A lot of these charges are avoidable, but they still catch people because the rules are easy to miss or tied to small account requirements. A bank account should not feel difficult to maintain just to avoid basic fees.

If you want accounts designed to avoid these charges altogether, it helps to compare the best no-fee banks.

Why Interest Rates Matter

Your savings rate plays a big role in how quickly your money grows, especially if you keep adding to your balance over time.

Even a 1% difference in APY can mean an extra $100+ per year on a $10,000 balance. A higher savings rate is one of the easiest ways to earn more from money you are already keeping in savings.

This matters most for emergency funds, short-term savings goals, or cash that may stay parked in your account for a while.

What “No-Fee” Really Means

Some banks advertise “no fees,” but there are often requirements attached to that claim.

Common conditions may include:

- Setting up direct deposit

- Keeping a minimum balance

- Making a certain number of debit card transactions

That does not automatically make the account bad, but it is important to understand the rules before opening it. In general, the easiest accounts to live with are the ones that do not require constant attention just to avoid charges.

Bank Features That Matter Most

The best banking features are usually the ones that make your money easier to handle without creating extra work.

Most banks offer similar basic accounts, so the biggest difference often comes down to how the account feels to use once it becomes part of your everyday routine.

Mobile App and User Experience

A good banking app matters more than most bonus features. If an app is slow, cluttered, or frustrating to use, it becomes harder to keep up with your accounts regularly.

A strong banking app should make it easy to:

- Check balances quickly

- Move money between accounts

- Deposit checks

- Review transactions

- Set alerts or notifications

For many people, the app becomes the main way they interact with their bank, so even small annoyances start to stand out over time.

Automation and Account Tools

Automation is one of the biggest advantages modern banks offer. Features like direct deposit, recurring transfers, and automatic savings can help keep your money organized without having to think about it constantly.

Helpful banking tools can include:

- Automatic savings transfers

- Spending alerts

- Recurring bill payments

- Savings buckets or goals

- Early direct deposit

None of these features are life-changing on their own, but together they can make banking feel a lot smoother month to month.

Account Structure and Organization

How your accounts work together matters more than most people realize.

For example, using checking for spending and savings for goals or emergency funds creates a clearer separation between money you can use freely and money you are trying to hold onto.

A connected setup also makes transfers and tracking easier because everything works together instead of being spread across several unrelated accounts.

The goal is not to find the bank with the longest feature list. It is to find one that fits naturally into how you already manage your money.

Read: What to Look for in a Checking Account Before Opening One

How to Choose a Bank That Fits Your Lifestyle

Even a good bank account can become frustrating if it does not match how you actually handle money day to day.

The best setup usually depends less on what looks good on paper and more on how you bank in real life.

ATM Access and Cash Needs

If you rarely use cash, ATM access may not matter very much. But if you pull out cash often, limited ATM access or repeated out-of-network fees can get old fast.

It helps to think about:

- How often you use cash

- Whether you deposit cash regularly

- If you travel often

- Whether branch access is important to you

For a lot of people, online banks work perfectly well without branches. But if cash is part of your routine, a traditional or hybrid bank may end up being the better fit.

Customer Support and Reliability

Most of the time, banking stays in the background. But when something breaks, customer support suddenly matters a lot.

Problems like:

- Fraud alerts

- Locked debit cards

- Transfer delays

- Login issues

- Disputed charges

can turn into a headache quickly if support is hard to reach or slow to respond.

A bank should make problems easier to fix, not harder to deal with.

Security and FDIC Insurance

A bank should always be FDIC-insured or backed by an FDIC-insured institution. FDIC coverage protects deposits up to at least $250,000 per depositor, per ownership category.

This becomes especially important with online banks or newer financial apps where it is not always obvious which institution is actually holding your money.

It is also worth looking at security features like transaction alerts, account monitoring, and multi-factor authentication. These tools can help catch suspicious activity early before it becomes a bigger problem.

The best bank for someone else may not work as well for you. A setup that matches your habits and daily routine is usually easier to stick with long term.

Bank Checklist: What to Look For

Before opening a bank account, it helps to look at a few basics that can quickly tell you whether a bank is likely to fit your needs or not.

A good bank setup will usually include:

- No monthly maintenance fees

- Competitive savings rates

- A clean, reliable mobile app

- Easy transfers and automation

- ATM or branch access that fits your routine

- Good customer support

- FDIC insurance protection

If a bank falls short in several of these areas, there is a good chance it will become more frustrating or expensive to deal with over time.

The goal is not to find a “perfect” bank. It is to find one that works well for how you already manage your money and does not create unnecessary problems later.

Common Mistakes When Choosing a Bank

A lot of people pick a bank based on convenience, familiarity, or a sign-up bonus without thinking much about how the account will actually work long term.

That often leads to small frustrations that become harder to ignore over time.

Choosing a Bank Based Only on Brand Name

Large banks often feel more established or trustworthy, but bigger does not automatically mean better.

Some national banks still offer low savings rates, higher account fees, or outdated apps compared to newer online banks. The name on the building matters a lot less than whether the account fits how you manage your money.

Ignoring Fees and Savings Rates

Monthly fees and low savings rates are easy to brush off because the numbers seem small at first.

But even a $10 monthly fee adds up to $120 per year, and low APYs can quietly cost even more in lost savings growth over time.

Opening Too Many Accounts

Having multiple bank accounts is not necessarily bad, but too many disconnected accounts can make banking harder to keep track of.

It becomes easier to miss transfers, forget where money is sitting, or bounce between apps just to figure out what is happening.

If you are not sure how many accounts actually make sense, it helps to understand how many bank accounts you should have before opening more.

Choosing Based Only on Sign-Up Bonuses

Bank bonuses can be useful, but they should not be the main reason you open an account.

A temporary $200–$300 bonus usually matters a lot less than long-term things like fees, savings rates, app quality, and how easy the account feels to use month after month.

Not Thinking About How Accounts Work Together

One of the most common mistakes is opening accounts one at a time without thinking about how everything fits together.

A setup usually works better when checking, savings, automation, and spending all connect in a way that feels easy to manage.

The best banking setup is rarely the most complicated one. Most of the time, the setup that works best is the one you can keep organized without constantly dealing with it.

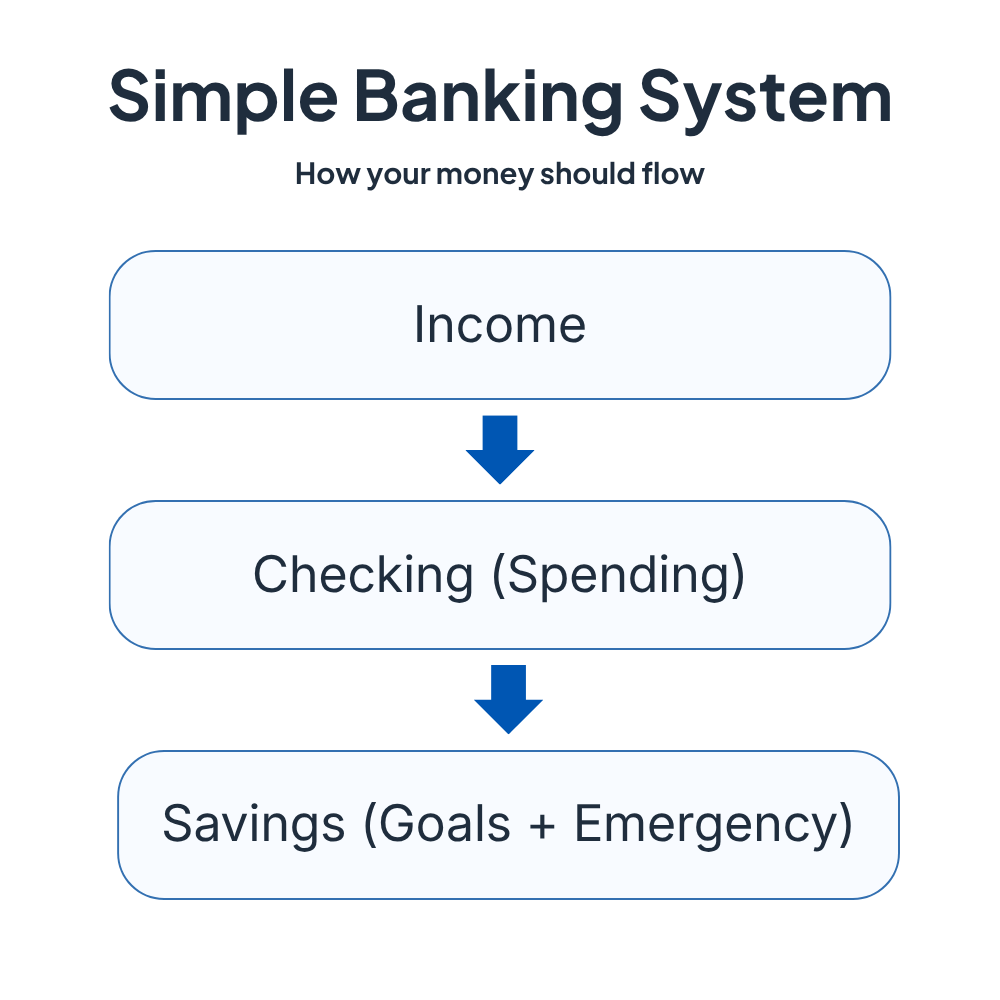

How to Set Up a Simple Banking System

A simple banking setup is usually easier to keep organized and far less frustrating to deal with over time.

For most people, a solid setup starts with:

- One checking account for spending and bills

- One savings account for emergency funds or goals

- Automatic transfers between accounts

That is enough for everyday banking without turning your setup into something complicated.

Use Checking and Savings for Different Jobs

Checking works best for spending, bills, and direct deposits, while savings works better for emergency funds, short-term goals, or money you do not want mixed into daily spending.

Keeping those roles separate makes it easier to tell what money is available and what money should stay alone.

Automate as Much as Possible

Automation takes a lot of the mental effort out of managing money.

Automatic transfers, direct deposit splits, and recurring bill payments help keep everything moving without needing constant attention.

Even basic automation can make saving feel more consistent because the money moves before you have a chance to spend it somewhere else.

Avoid Making Your Setup Too Complicated

A lot of people end up opening extra accounts they do not really need.

More accounts can sometimes help with organization, but too many can create extra logins, more transfers, and more things to track every month.

For most people, a smaller setup with clear roles works better than a complicated system that feels difficult to stay on top of.

If you want a deeper breakdown of how accounts can work together, it helps to understand how many bank accounts you should have as your setup grows.

The goal is not to build a perfect banking system. It is to create one that works well without constantly needing your attention.

If you want a simple example of how this can work in practice, you can see how the Savefinity System organizes banking, budgeting, saving, and investing into one connected setup.

Final Thoughts on Choosing the Right Bank

Read: Best Banks for our top overall banking picks.

Choosing the right bank usually comes down to finding one that fits the way you already manage your money. Over time, low fees, strong savings rates, a reliable app, and an account that feels easy to manage tend to matter more than temporary bonuses or extra features you may never use.

For most people, banking gets easier when the setup stays simple. A good bank should make it easier to save, spend, and stay organized month to month — not create more accounts, extra steps, or additional things to keep track of.