50/30/20 Budget Rule Explained

Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you.

Budgeting usually feels more complicated than it needs to be. Between spreadsheets, budgeting apps, and detailed tracking systems, a lot of people end up giving up before they ever build a routine that actually lasts.

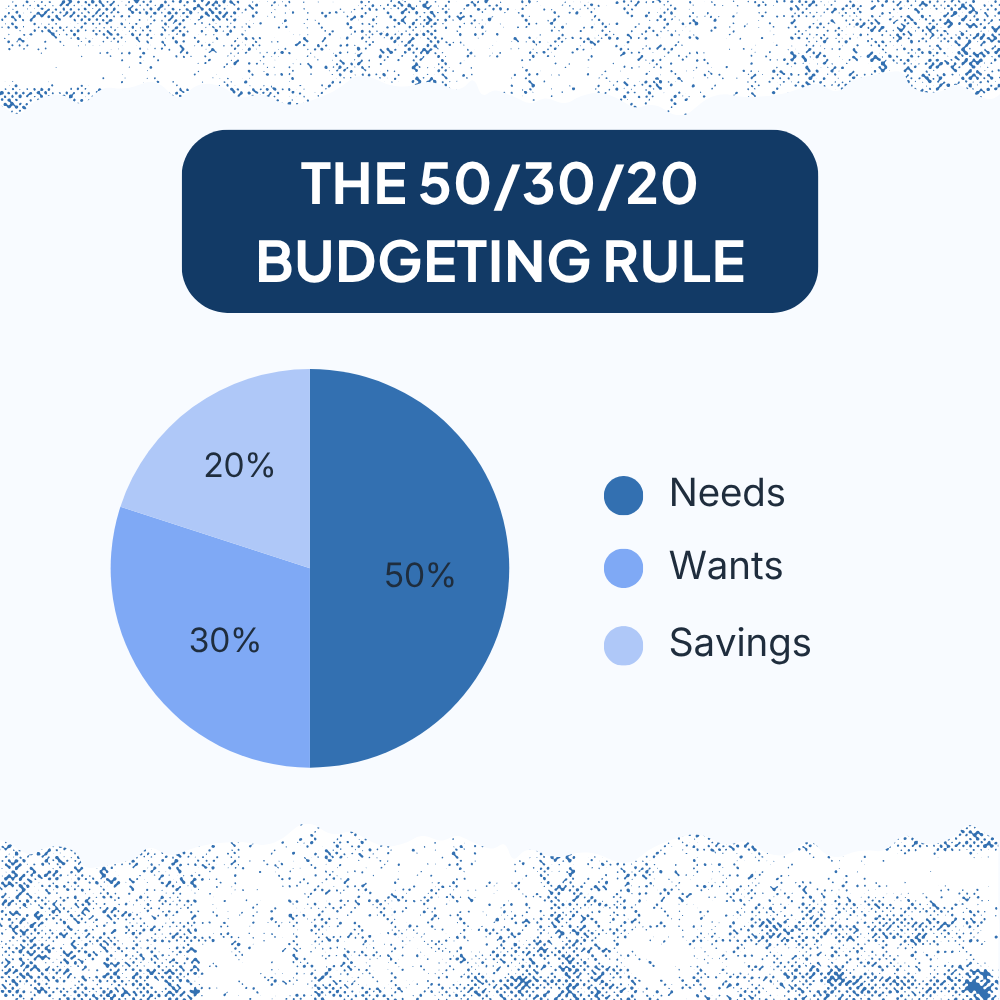

The 50/30/20 budget rule is a simple budgeting method that divides your after-tax income into three categories:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

Instead of tracking every dollar perfectly, the goal is to create a basic structure that helps you manage spending while still making financial progress over time.

For many people, the biggest advantage of the 50/30/20 budgeting rule is that it feels easier to stick with long term than stricter budgeting systems.

Read Best Budgeting Apps to see our top picks.

What Is the 50/30/20 Budget Rule?

The 50/30/20 budget rule is a budgeting method that separates your take-home income into three broad spending categories.

| Category | Percentage | Purpose | Example Monthly Amount ($4,000 Income) |

|---|---|---|---|

| Needs | 50% | Essential expenses | $2,000 |

| Wants | 30% | Lifestyle and flexible spending | $1,200 |

| Savings & Debt | 20% | Saving, investing, or debt payoff | $800 |

The goal is not budgeting perfection — it is creating a simple structure you can realistically maintain month after month.

The idea is to create a balance between spending, lifestyle flexibility, and long-term financial goals without making budgeting feel exhausting to maintain.

The 50/30/20 budget rule is often used as a beginner budgeting framework because it creates a simple monthly budget without requiring detailed expense tracking. For many people, it works as a starting point for organizing spending, saving, and debt repayment more consistently.

Unlike highly detailed budgets, the 50/30/20 method focuses more on overall spending patterns than perfect category tracking.

For example, if you bring home $4,000 per month after taxes, around half would typically go toward essentials, while the remaining amount gets split between lifestyle spending and future financial goals.

The percentages do not need to be exact every month. For most people, the system works better as a flexible guideline than a rigid formula.

How the 50/30/20 Budget Rule Works

The 50/30/20 budgeting rule works by separating spending into three major areas that cover most day-to-day financial decisions.

For many people, this approach feels less stressful because it avoids the constant tracking and micromanaging that often makes traditional budgets hard to maintain.

If you are building your first budget, it can also help to learn how to start a budget in a way that feels realistic to maintain long term.

50% for Needs

Needs are the expenses you realistically have to pay in order to live and work.

Common examples include:

- Rent or mortgage

- Utilities

- Groceries

- Insurance

- Transportation

- Minimum debt payments

- Phone bill

- Basic healthcare costs

The key difference is that needs are essential expenses — not simply things you use often.

For example, groceries are usually considered a need. Frequent restaurant meals are usually considered wants.

One of the most common budgeting mistakes is treating too many expenses like necessities. That can make a budget feel tighter than it actually is. For example, premium subscriptions, newer car payments, or frequent convenience spending often get treated like fixed expenses even though there is usually more flexibility there than people realize.

30% for Wants

Wants are non-essential expenses that improve your lifestyle or entertainment but are not strictly necessary.

This category often includes:

- Dining out

- Streaming services

- Shopping

- Hobbies

- Vacations

- Entertainment

- Gym memberships

- Upgraded subscriptions

The wants category matters more than people sometimes realize. Budgets that remove all enjoyable spending often become difficult to maintain once the early motivation fades. Even setting aside a modest amount for dining out, hobbies, or entertainment can make a budget feel much more sustainable month to month.

A budgeting system usually works better when it leaves room for everyday life instead of trying to eliminate every flexible expense.

20% for Savings and Debt Repayment

The final 20% usually goes toward improving your financial position over time.

This category can include extra savings, investing, and debt payments beyond required minimums:

- Emergency fund savings

- Retirement investing

- Extra debt payments

- Brokerage investing

- Long-term savings goals

For people with high-interest debt, a larger portion of this category may temporarily go toward extra debt payoff before shifting more heavily toward savings or investing later. Minimum debt payments usually belong in the needs category because they are required monthly expenses.

For people building an emergency fund for the first time, it can also help to understand how high-yield savings accounts work and why many people separate savings from everyday spending accounts. Keeping emergency savings separate from checking often reduces the temptation to spend money that is meant for unexpected expenses.

The goal is to make consistent progress instead of trying to optimize every dollar perfectly from the beginning.

50/30/20 Budget Example

Here is a simple example using a monthly take-home income of $5,000.

| Category | Percentage | Monthly Amount | Example Expenses |

|---|---|---|---|

| Needs | 50% | $2,500 | Housing, groceries, insurance |

| Wants | 30% | $1,500 | Dining out, entertainment, shopping |

| Savings & Debt | 20% | $1,000 | Emergency fund, investing, debt payoff |

In real life, very few budgets fit these percentages perfectly every month.

For example, someone living in a high-cost city may spend closer to 60% on needs once housing, transportation, and insurance are included. Someone aggressively paying off credit card debt with interest rates around 20%–30% may temporarily direct far more than 20% toward debt reduction instead of investing.

That does not automatically mean the budget is failing. The percentages are mainly meant to help you understand where your money is going.

One reason the 50/30/20 method continues to work for many people is that it focuses more on consistency than precision. Instead of building a complicated system that becomes difficult to maintain, the structure keeps budgeting simple enough to realistically follow month after month.

Why the 50/30/20 Rule Became Popular

The 50/30/20 budget rule is commonly used because it gives people a simple financial structure without requiring constant expense tracking.

A lot of budgeting systems fail because they eventually become exhausting to manage. Tracking dozens of spending categories every week can start to feel like extra work people eventually stop keeping up with.

The 50/30/20 method simplifies budgeting by focusing on broad priorities instead of perfect precision.

For many people, the biggest advantages are:

- Easier to maintain long term

- Less time spent tracking purchases

- Flexible enough for changing expenses

- Creates balance between spending and saving

- Helps prevent overspending without extreme restriction

This is also why the system works well for beginners who want a starting point without immediately jumping into highly detailed budgeting methods.

Is the 50/30/20 Budget Rule Realistic?

The 50/30/20 budget rule is realistic for some people, but not every income level or cost-of-living situation fits neatly into the percentages.

Housing costs are often the biggest challenge. In many cases, rent or mortgage payments alone can consume 30%–40% of take-home income before other basic expenses are added.

In higher-cost areas, rent or mortgage payments can take up a large share of income, which may push total needs above 50% once groceries, insurance, transportation, and utilities are included.

That does not necessarily make the system useless. It usually means the percentages need to be adjusted to fit real-world costs.

For example:

| Situation | Possible Budget Adjustment |

|---|---|

| High housing costs | 60/20/20 |

| Aggressive debt payoff | 50/20/30 |

| Lower income | 70/20/10 |

| High savings focus | 40/20/40 |

The overall structure usually matters more than forcing exact percentages.

The goal is understanding whether your spending is reasonably balanced — not squeezing your life into unrealistic budgeting numbers.

The Consumer Financial Protection Bureau budgeting guide also explains that budgeting systems often work better when they are flexible enough to fit real-world expenses and changing financial situations.

Income level also matters. Someone earning $40,000 per year may have very different budgeting pressure than someone earning $120,000, even if they use the same percentages. The rule tends to work best when basic living expenses leave enough room for savings and flexible spending without constantly feeling restrictive.

Common Problems With the 50/30/20 Budget Rule

Even though the system is simple, there are still a few areas that regularly create confusion.

Misclassifying Expenses

Some expenses fall into gray areas depending on how they are used.

For example:

| Expense | Need or Want? |

|---|---|

| Basic internet | Usually a need |

| Luxury car payment | Often a want |

| Groceries | Need |

| Frequent takeout | Usually a want |

| Basic clothing | Need |

| Designer shopping | Want |

The goal is not perfect categorization. It is being reasonably honest about which expenses are truly essential versus more flexible.

Ignoring Irregular Expenses

A lot of people build monthly budgets while forgetting occasional costs like:

- Car repairs

- Holidays

- Annual subscriptions

- Medical expenses

- Travel

- Home maintenance

Without planning for these expenses, a budget can look balanced on paper while still causing financial stress throughout the year. Even setting aside a small amount monthly for irregular costs can make larger expenses feel much more manageable when they eventually happen.

Making the Budget Too Restrictive

One reason many budgets fail is because they remove too much flexibility too quickly.

If every dollar feels tightly controlled, people often abandon the system entirely after a few weeks.

The 50/30/20 budgeting method usually works better when it stays simple and realistic enough to maintain consistently.

50/30/20 Budget Rule vs Zero-Based Budgeting

The 50/30/20 budget rule and zero-based budgeting are very different approaches to managing money.

| 50/30/20 Budget Rule | Zero-Based Budgeting |

|---|---|

| Simpler structure | More detailed |

| Flexible categories | Every dollar assigned |

| Faster to maintain | More hands-on |

| Easier for beginners | Better for tighter budgeting |

| Less precise | More control |

Zero-based budgeting works well for people who want maximum control over every dollar.

The 50/30/20 method usually works better for people who want a simpler budgeting system that still creates financial structure without constant tracking.

If you want a more detailed budgeting approach, it also helps to understand how zero-based budgeting works and how it compares to more flexible systems.

Tips for Following the 50/30/20 Budget Rule

The 50/30/20 budgeting rule usually works best when it stays simple.

A few small adjustments often make budgeting feel much easier to maintain over time.

Automate Savings First

Automatic transfers help remove a lot of the decision-making from budgeting.

For example:

- Direct deposit splits

- Automatic savings transfers

- Recurring investment contributions

- Automatic debt payments

Automation reduces the chance that money gets spent before it reaches savings goals.

Focus on Large Expenses First

Reducing a few larger expenses usually matters more than obsessing over tiny purchases. Lowering a monthly housing payment by even $200 usually has a bigger long-term impact than trying to cut a few dollars from occasional small purchases.

For example, lowering:

- Housing costs

- Car payments

- Insurance premiums

- Subscription overload

often has a larger financial impact than trying to cut every small discretionary purchase.

Keep the System Flexible

Budgets usually work better when they can adapt to real life.

Some months naturally come with travel, medical bills, higher utilities, or unexpected expenses. A flexible budgeting system is often easier to maintain than one that expects perfect consistency every month. For many people, the percentages work best as monthly averages rather than strict weekly targets.

A budget usually works better when it supports your routine instead of constantly fighting against it.

Who the 50/30/20 Budget Rule Works Best For

The 50/30/20 budgeting rule often works well for:

- Beginners learning how to budget

- People who dislike detailed tracking

- Moderate or stable income households

- People looking for a simpler budgeting structure

- Anyone trying to balance spending and saving more consistently

It may work less effectively for:

- Highly variable incomes

- Extremely tight budgets

- Aggressive debt payoff plans

- Self-employed or commission-based income

- Complex financial situations

In those situations, more detailed budgeting systems sometimes work better because income and expenses may change significantly from month to month.

50/30/20 Budget Rule FAQ

Is the 50/30/20 budget rule based on gross income or net income?

The 50/30/20 rule is usually based on after-tax income, also called take-home pay. That gives a more realistic picture of the money you actually have available each month.

What if my needs are more than 50%?

That is common, especially in higher-cost areas. The percentages are guidelines, not strict rules. In many cases, adjusting the ratios is more realistic than forcing exact percentages.

Does the 20% include retirement investing?

Yes. The savings category can include emergency funds, retirement contributions, investing, or extra debt payments. If retirement contributions already come out of your paycheck before you calculate take-home pay, just make sure you are counting them consistently.

Is the 50/30/20 rule good for beginners?

For many people, yes. The structure is simple enough to understand quickly without requiring constant expense tracking.

Can the 50/30/20 budget rule help you save money?

Yes. For many people, a simpler budget works better long term because it is easier to consistently follow. Even small improvements — like saving an extra $100 per month — can add up over time.

Can you use the 50/30/20 rule with budgeting apps?

Yes. Many budgeting apps can automatically group expenses into categories that roughly match the system. If you are comparing options, it can help to review some of the best budgeting apps for different budgeting styles.

Is the 50/30/20 Budget Rule Right for You?

Read Best Budgeting Apps to see our top picks.

The 50/30/20 budget rule works because it simplifies budgeting into a structure most people can realistically maintain.

Instead of focusing on perfect tracking, the system helps you become more aware of spending, saving, and overall financial balance. That usually makes budgeting feel less overwhelming while still encouraging better money habits over time.

For many people, the best budgeting system is not the most detailed one. It is the one that feels simple enough to follow consistently while still helping you save, spend, and plan more intentionally over time.

If you want to build a more complete money setup around budgeting, saving, and automation, it can also help to learn how the Savefinity System organizes banking, budgeting, investing, and protection into one connected setup.