How Many Bank Accounts Should You Have?

Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you.

How many bank accounts should you have? For most people, the answer is 2–3 accounts—typically one for spending, one for savings, and sometimes a separate account for bills.

Using the right number of bank accounts makes it easier to manage your money, separate spending from saving, and stay consistent over time. In this guide, you’ll learn exactly how many bank accounts you need, how to structure them, and the simplest way to set up a system that works in real life.

How Many Bank Accounts Should You Have? (Simple Answer)

The right number of bank accounts depends on how you manage your money, but there’s a clear range that works for most people:

- 1 account: simplest setup, but limited control

- 2–3 accounts: ideal for most people

- 4+ accounts: more advanced organization

From a practical standpoint, more accounts only make sense if they solve a specific problem. If they don’t improve how your money is managed, they usually just add friction—so for most people, starting with 2–3 accounts is the easiest and most effective place to begin.

If you’re still deciding where to keep those accounts, it helps to understand how to choose the right bank before setting everything up.

Read Best Banks to see our top picks.

A Simple Bank Account Breakdown

Most people fall into one of three simple setups depending on how they manage their money.

Here’s a simple breakdown of each setup and when it makes sense:

| Setup Type | Number of Accounts | Best For |

|---|---|---|

| Basic | 1 | Simplicity, minimal management |

| Standard | 2–3 | Most people, balanced setup |

| Advanced | 4+ | Detailed organization, multiple goals |

Most people fall into the 2–3 account range because it provides enough separation between spending and saving without becoming hard to manage, making it the most practical starting point if you’re unsure what setup to use.

A single account can work early on, but it often leads to mixing bills, spending, and savings—once you have more than 2–3 recurring expenses, this usually becomes harder to manage. On the other end, having too many accounts (5+) can make transfers, tracking, and automation harder than necessary.

Why Multiple Bank Accounts Can Help

Using more than one account isn’t about complexity—it’s about clarity.

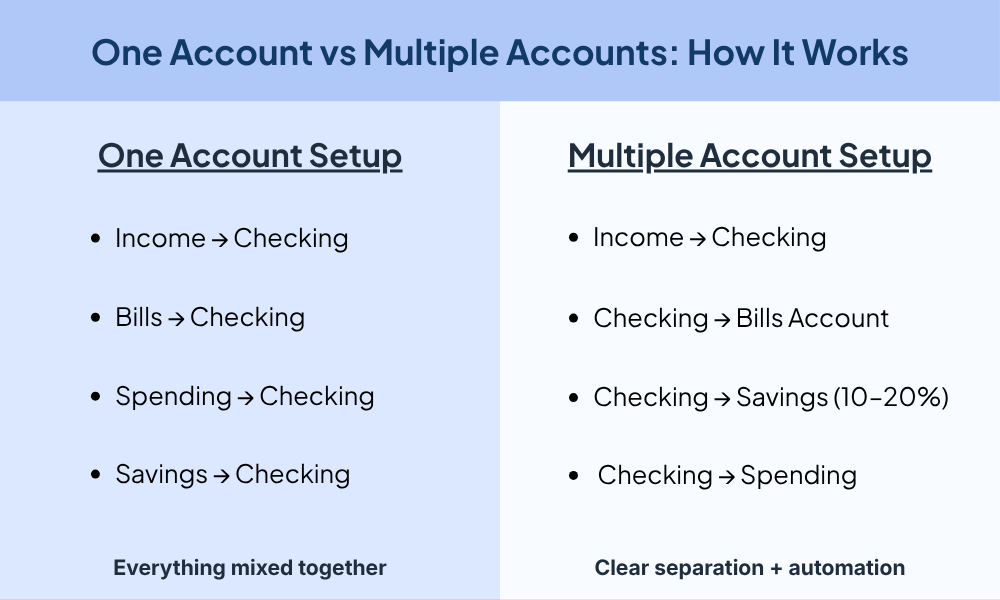

Separating your money into different accounts makes it easier to see what you can spend, what needs to be saved, and what’s already committed to bills. In practice, this usually matters when your balance looks “high” but a large portion is already spoken for—separating accounts removes that confusion and helps prevent overspending.

For example, having $2,000 in one account can feel like plenty until $1,500 of it is already needed for bills, which is where separate accounts make a clear difference.

It also makes automation much easier. You can set up transfers so money moves automatically between accounts—like sending 10–20% of your income to savings or keeping bills separate from daily spending. This reduces manual tracking and makes saving more consistent over time.

Here’s what that looks like in practice:

A simple example of how separating accounts makes money easier to manage.

In most cases, this leads to:

- Better control over spending

- More consistent saving

- Fewer mistakes like overdrafts or missed payments

What we found is that even adding just one extra account (like a savings account) can noticeably improve consistency, particularly when you’re setting aside $100–$500 per month toward savings goals.

The Ideal Bank Account Setup for Most People

For most situations, a simple 2–3 account setup works best. It keeps your spending, saving, and bills clearly separated without adding unnecessary complexity, which is why it works well for most people.

In practice, this setup creates a basic system where each account has a clear purpose, making your money easier to manage and reducing the chances of mistakes.

1. Checking Account (Daily Spending)

This is your main account for income, bills, and everyday purchases. It acts as the hub where your money flows in and out.

Keeping all daily spending in one place makes it easier to track and manage without overthinking it, which is why this is the foundation of almost every effective setup.

2. High-Yield Savings Account (Savings & Emergency Fund)

A separate savings account is where you keep money you don’t want to touch regularly, such as an emergency fund of around $1,000 to start, then 3–6 months of expenses, along with other savings goals.

Based on how these typically work, keeping savings separate reduces the chance of dipping into it for everyday expenses. It also helps your money grow if the account earns interest, making this the first account most people should add after checking.

Many savings accounts also let you organize money into separate “buckets” or goals, which can make it easier to track different priorities without needing multiple accounts.

3. Optional: Bills Account

A third account can help if you want more structure by separating your fixed expenses from daily spending.

This is most useful if your bills vary month to month or if you want to make sure money for rent, utilities, and subscriptions is set aside ahead of time, reducing the risk of missed payments or overdrafts.

How to Decide How Many Bank Accounts You Need

The right number of bank accounts comes down to how your money is currently working—and where it’s breaking down.

Start by looking at your setup. If everything is in one account and your balance feels unclear—like when it swings by $500–$1,000 and you’re not sure what’s safe to spend—that’s a sign you need more separation.

Use these simple signals to guide your setup:

- Money feels mixed together → Add a separate savings account

- Bills are getting missed or tight → Add a bills account

- Saving isn’t consistent → Keep savings separate and automate transfers

- Everything already feels clear and controlled → You likely don’t need another account

In practice, most people only need 2–3 accounts because each one solves a specific problem—spending, saving, or organizing bills.

The goal isn’t to add more accounts—it’s to make your money easier to understand and manage day to day.

Simple Bank Account Setup Example

If you want a straightforward starting point, this works well for most people:

- Start with one primary checking account

Use this for income and everyday spending so everything flows through one place. - Add a high-yield savings account

Keep emergency savings separate to avoid accidental spending. - Separate emergency savings first

Focus on building a basic buffer of at least $500–$1,000 before adding more accounts. - Add extra accounts only if needed

Only expand your setup if it solves a real issue, like managing bills more clearly.

This approach keeps things simple while still giving you structure, making it a solid starting point if you’re setting up your accounts for the first time or simplifying an existing setup.

If you want a simple way to set up your money:

A simple 3-step system to organize, grow, and manage your money.

- Set up your full money system in minutes

- Automate saving, budgeting, and investing

- Built to keep your money simple and organized

We tested 40+ tools to build a system designed to simplify how you manage and grow your money.

Common Bank Account Mistakes to Avoid

Even with a solid setup, a few common mistakes can make your accounts harder to manage than they need to be. Most of these come down to either having too little structure or adding complexity without a clear purpose.

- Keeping everything in one account long-term

It may feel simple, but it often leads to confusion and inconsistent saving once your spending and bills start mixing together. - Opening too many accounts too quickly

More accounts don’t automatically mean better organization—especially if they aren’t used intentionally, which can make your setup harder to manage. - Not automating transfers

Without automation, it’s easier to forget or delay moving money where it needs to go—like consistently saving 10–20% of your income each month. - Choosing accounts with fees or low interest

Even a $10 monthly fee adds up to $120 per year, which can quietly slow your progress over time.

The goal isn’t to avoid multiple accounts—it’s to use them intentionally. A simple, well-structured setup will always work better than one that’s either too basic or unnecessarily complicated.

How Many Bank Accounts Should You Have Long Term?

Read Best Banks to see our top picks.

Most people only need 2–3 bank accounts to manage their money well. For many setups, that is enough to separate spending, saving, and bills without adding unnecessary complexity.

More accounts are not always better. They only help if they make your finances easier to organize and manage day to day. For most people, a simple setup with one checking account, one savings account, and sometimes a separate bills account is usually enough.

The goal is not to build the most advanced banking system possible. It is to create a setup that feels simple, organized, and easy to maintain over time. Starting with a basic system and adjusting later usually works better than creating something overly complicated from the beginning.