Checking vs Savings Account: Differences and Which You Need

Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you.

Checking vs savings accounts mostly comes down to how you use your money. A checking account is built for everyday spending, bill payments, debit card purchases, and direct deposits, while a savings account is designed for storing money separately and earning interest over time.

For most people, using both accounts together creates a simpler and more organized banking setup. Keeping spending money separate from savings often makes budgeting, emergency funds, and automatic saving easier to manage long term.

Checking vs Savings Accounts: What’s the Difference?

The difference between checking vs savings accounts is that checking is used for everyday spending, while savings is used to store money and earn interest.

A checking account lets you spend, pay bills, and move money easily. A savings account keeps money separate and helps it earn interest over time. For most people, this difference matters because it creates a clear line between money you can spend today and money you’re trying to keep.

Quick takeaway: use checking for day-to-day money, and savings for money you don’t plan to spend right away.

Here’s a quick side-by-side comparison:

| Account Type | Best Use | Access | Interest |

|---|---|---|---|

| Checking | Daily spending | Very easy (card/app) | 0.00%–0.10% APY |

| Savings | Saving money | Limited/friction | ~3.00%–5.00% APY |

Checking = access and spending. Savings = growth and separation.

Read Best Banks to see our top picks.

What Is a Checking Account?

A checking account is designed for everyday money use. This is where your income usually goes, and where your bills and daily purchases come from.

This is the account you’ll use the most. It’s built for speed and convenience—debit cards, transfers, and bill payments all happen here. In practice, this becomes your “daily money” account, so it works best when you only keep what you plan to spend.

When a Checking Account Makes Sense

A checking account works best when you need quick, consistent access to your money.

- Paying monthly bills like rent, utilities, or subscriptions

- Daily spending like groceries, gas, or online purchases

- Receiving income through direct deposit

Most people rely on checking as their “main hub” for incoming and outgoing money. This works best if you keep it limited to short-term spending, not long-term savings.

Limits and Trade-Offs

The trade-off is that checking accounts typically don’t help your money grow.

- Interest rates are usually near 0.00%–0.10% APY

- Easy access can make it easier to spend without thinking

This usually becomes your “daily money” account, so it works best when you only keep what you plan to spend.

What Is a Savings Account?

Read What Is a High-Yield Savings Account.

A savings account is designed to hold money you don’t need to spend right away. Its main purpose is to keep your money separate and allow it to earn interest.

Unlike checking, savings accounts create a small barrier between you and your money. That friction helps protect it from everyday spending. For most people, this separation is what actually makes saving work consistently.

When a Savings Account Makes Sense

Savings accounts are best used for money you want to keep but not touch frequently.

- Building an emergency fund (often 3–6 months of expenses)

- Saving for short-term goals like travel or large purchases

- Holding extra cash that isn’t needed for daily use

This separation is what makes savings accounts effective—they reduce the temptation to spend. This usually matters most if you’ve struggled to keep money set aside in the past.

Limits and Trade-Offs

Savings accounts are not designed for frequent use.

- Withdrawals may be limited by your bank or made less convenient

- No debit card or limited payment features

That slight inconvenience is actually a benefit—it helps protect your savings from being used casually.

Key Differences Between Checking and Savings Accounts

Read How Many Bank Accounts Should You Have.

The differences between checking vs savings accounts go beyond just “spending vs saving.” They affect how you manage your money day to day.

Here’s a simple visual comparison of how they differ:

| Feature | Checking | Savings |

|---|---|---|

| Access | High | Low |

| Interest | Low | High |

| Spending | High | Low |

The table gives a quick overview, but each difference matters in how you actually use these accounts day to day.

Access:

Checking accounts allow instant access through cards, apps, and payments. Savings accounts often require transfers first, which can take 1–2 business days depending on the setup.

Interest:

Checking accounts usually earn little to no interest. Savings accounts often offer higher rates (around 3.00%–5.00% APY), which can make a noticeable difference over time, especially on balances over $1,000. This matters most if you’re holding extra cash, since leaving it in checking can quietly cost you growth.

Usage:

Checking is meant for frequent use—multiple transactions per week or day. Savings is used occasionally, mainly for deposits and occasional withdrawals.

Behavior impact:

Keeping everything in checking makes it easier to spend without realizing it. Separating money into savings creates a clearer boundary and helps you hold onto it.

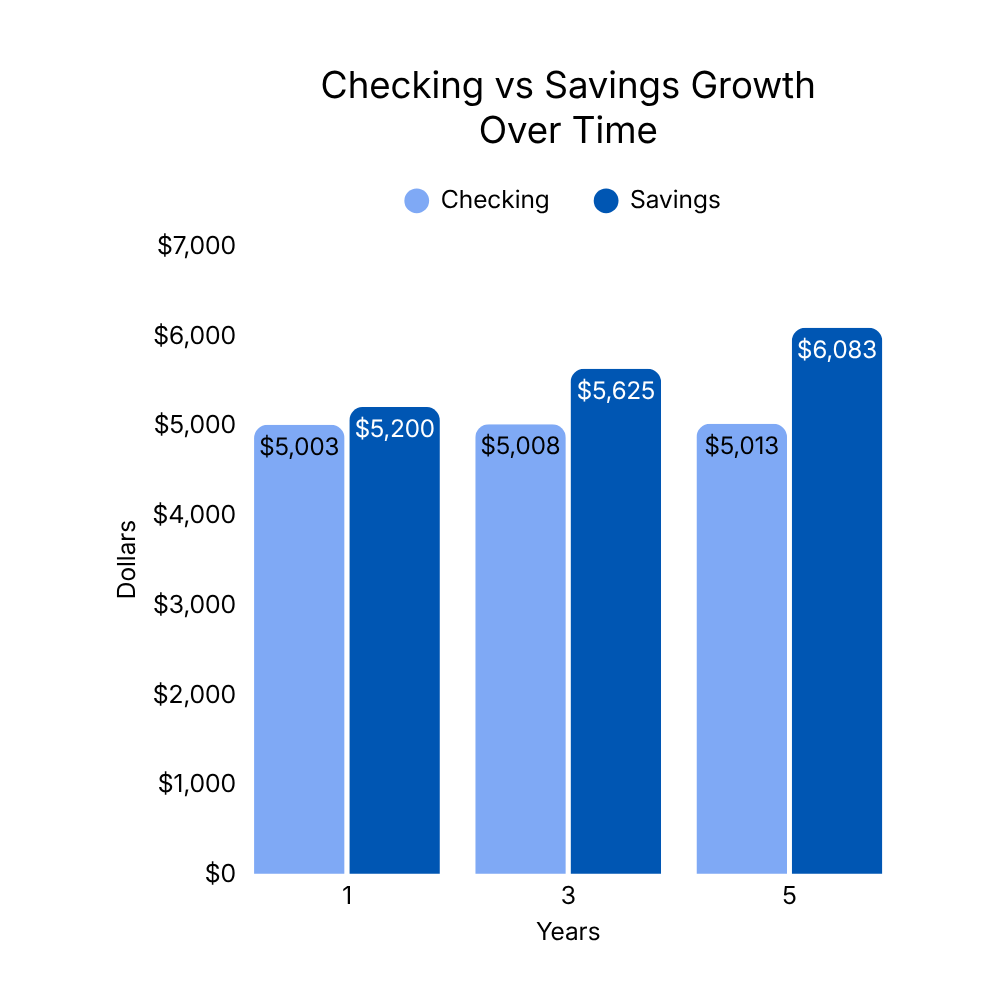

For example, someone keeping $5,000 in checking may slowly spend it down. Keeping that same $5,000 in savings earning around 4.00% APY could add about $200 per year while keeping it separate from spending.

Do You Need Both Accounts?

For most people, using both accounts is the simplest and most effective setup.

A single account can technically work, but it usually creates confusion between spending and saving. When everything is in one place, it’s harder to tell what’s safe to spend. For most people, this is where money slowly gets used without a clear plan.

Can You Use Just One Account?

You can use only a checking or only a savings account, but it tends to create problems over time.

- Using only checking often leads to overspending

- Using only savings makes everyday transactions inconvenient

In most cases, the lack of separation is what causes issues—not the account itself. This setup works best when you want a simple system that keeps spending and saving clearly separated.

Simple Setup That Works

A basic two-account setup keeps things clear and easy to manage.

- Checking: income, bills, and daily spending

- Savings: emergency fund and goals

- Transfers: move extra money (even $50–$200 per paycheck) from checking to savings regularly

This setup doesn’t require complexity—it just creates structure. For most people, this is the best default starting point.

Simple Checking and Savings Account Setup Example

A simple flow helps make this clear:

- Paycheck goes into checking

- Bills and everyday spending come from checking

- Extra money (for example, $100–$500 per month) is moved into savings

- Savings stays untouched unless needed

This creates a system where your spending and saving don’t compete with each other.

How to Choose the Right Checking and Savings Setup

The right setup doesn’t need to be complicated, but a few factors make a big difference.

The best setups usually come down to simplicity and cost.

- No fees: Avoid accounts with monthly or minimum balance fees

- Strong savings rate: Even a 1% difference (for example, 2% vs 4%) can add $100+ per year on a $5,000 balance

- Easy transfers: Moving money between accounts should be quick and simple

If you’re setting this up for the first time, it helps to start with a bank that offers both accounts in one place. This makes transfers easier and keeps everything organized. For most people, this is the simplest starting point before considering more complex setups.

Starting with a simple setup like this makes your money easier to manage and easier to stick with over time.

Common Checking and Savings Account Mistakes to Avoid

Most issues with checking vs savings accounts come from how they’re used, not the accounts themselves. In practice, small setup mistakes tend to have a bigger impact than the bank you choose.

- Keeping all money in checking, which makes it easy to overspend

- Ignoring interest rates and missing out on growth

- Using savings like a spending account, which defeats its purpose

- Not separating money, making it harder to track what’s available

Even small changes—like moving $25–$100 into savings weekly—can fix most of these problems.

Checking vs Savings Account FAQs

Can I use a savings account like a checking account?

You can, but it’s not ideal. Savings accounts aren’t designed for frequent transactions, and using them that way removes the benefit of separation.

Do I need both checking and savings accounts?

In most cases, yes. Using both helps separate spending from saving and makes your money easier to manage.

Which account earns more interest?

Savings accounts almost always earn more interest than checking accounts.

Are there limits on savings withdrawals?

Some banks limit certain types of withdrawals or make them less convenient. Even when limits are relaxed, savings accounts are still designed for occasional use.

Choose a Banking Setup That Fits How You Manage Money

Read Best Banks to see our top picks.

When comparing checking vs savings accounts, the difference is straightforward: checking is for using money, and savings is for holding and growing it.

Most people benefit from using both together. It keeps spending and saving separate, makes your money easier to manage, and helps avoid common mistakes. If you’re unsure where to start, this two-account setup is usually the simplest and most effective default.

The simplest setup is often the most effective—one account for daily use, and one for everything you want to keep. If you’re setting this up, you can compare options in our best banks guide.